What is a Section 1042 Election?

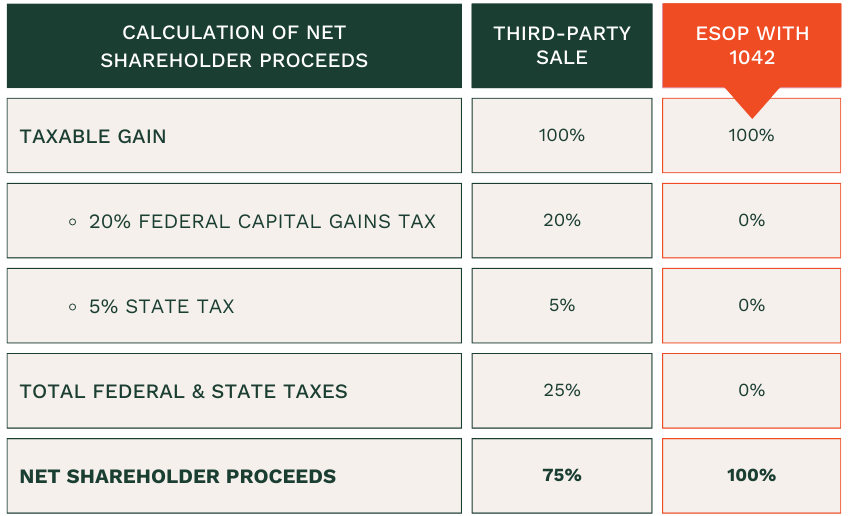

A Section 1042 election enables shareholders to eliminate capital gains tax on the sale of their company to an Employee Stock Ownership Plan (ESOP). Depending on your state tax rate, sellers will save between 20% and 33% as compared to a taxable sale. Enacted into law in 1986, Section 1042 was designed to incentivize business owners to transition ownership to their employees through an ESOP.

How Section 1042 Tax Deferral Works

A Section 1042 election allows the selling shareholder to defer capital gains tax by “rolling over” the proceeds from the sale of stock into Qualified Replacement Property (QRP). This rollover must take place within 12 months after the sale.

Think of the 1042 election as similar to a 1031 exchange in real estate, where the seller can defer taxes by reinvesting in a like-kind property. For 1042, the shareholder sells their stock in the company to an ESOP and reinvests the proceeds into QRP.

Section 1042 Requirements: What Business Owners Need to Know

To qualify for a Section 1042 election, certain criteria must be met.

- 30% Ownership: The ESOP must own at least 30% of the company after the transaction.

- Holding Period: Minimum 3-year ownership period for stock sold to the ESOP

- Corporate Structure: The company must be a C corporation at the time of the sale. Lazear’s tax strategists are experts in leading our clients who are not presently C corporations through a C corporation conversion to enable a 1042 election.

Maximizing an ESOP Transaction with Section 1042

For business owners considering an ESOP, understanding the potential tax savings from a Section 1042 election is a critical step in planning for a successful transaction.

Learn why Section 1042 was created and how business owners can defer capital gains taxes.

Explore Lazear’s proprietary 1042 tax solution by clicking here.